Today following the bell, Intel reported its third-quarter financial performance, including revenue of $14.5 billion and earnings per share of $0.64. Following its earnings beat, shares in the chip giant initially rose.

Analysts had expected Intel to report a $0.59 per-share profit, off revenue of $14.2 billion. Those expectations represented a 10.6 percent decline and a 2.3 percent fall, respectively.

To round out the raw numbers, Intel reported third-quarter net income of $3.1 billion and gross margin of 63 percent. The firm spent $1.1 billion on dividends during a three-month period, and repurchased 36 million of its own shares at an expense of $1.0 billion.

Breakdown

Numbers are god but also bullshit. So let’s take this apart slightly:

- Revenue from its PC group totaled $8.5 billion, which were up a strong 13 percent from its sequentially preceding quarter. While that is dandy, Intel’s Client Computing group brought in a full 7 percent less revenue than the year-ago quarter. PCs remain weak. We knew this.

- Each of Intel’s other groups grew sequentially, and two of three grew on a year-over-year basis. That’s to say that everything that Intel is doing that is not sticking chips into laptops is doing at least all right. Its software group was the weakest, while its data center group grew 8 percent sequentially, and 12 percent compared to the year-ago quarter.

- And at $4.1 billion in revenue, the data center cadre is Intel’s second-largest group.

Intel concluded the period with cash, equivalents, and short-term investments of more than $14 billion, up from the year-ago period, and the sequentially preceding quarter. So that’s nice.

The PC Market

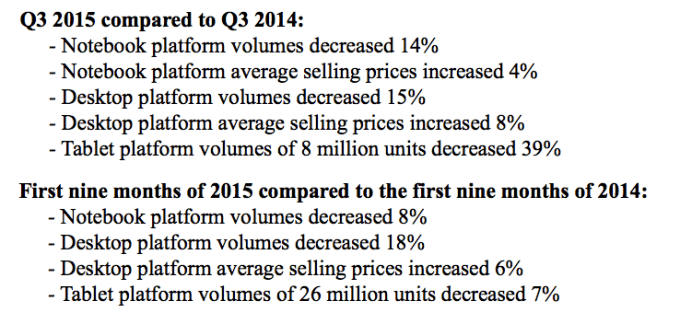

Please make the following sound with your face: Womp, womp. Here’s the breakdown via Intel’s release:

That’s not so good. Keep in mind that the PC market is large, with many players. The above means that other OEMs, and participants like Microsoft, likely aren’t have a ball.

Guidance

Call it outlook if you will, but Intel expects revenue of $14.8 billion in the holiday quarter. Presumably a chunk of that will come from the traditionally strong PC sales cycle that takes place around Christmas.

Intel expects its gross margin to slip 100 basis points to a round figure of 62 percent. Those figures imply profitability not wildly different from the now-past quarter.

Intel remains a company in transition, looking to new revenue streams to supplement and replace falling PC incomes; the decline of its PC dollars is not Intel’s fault, per se, but is instead more of a reflection on the stale, and slipping PC market itself.

Shares of Intel are now mostly flat in after-hours trading.

No comments:

Post a Comment